Upstream Intel 4/21/25

Declining Haynesville land | M&R heats up | EIA job cuts risk data quality | USEDC has $600m left for 2025 M&A | Industry bristles under policy changes

Welcome back to Upstream Intel, Lease Analytics’ weekly roundup of our analysis and insights. As always, we would love to hear from you with news ideas, feedback and anything else you find interesting.

Sent this by a friend? Sign up here to receive UIW in your inbox.

Data Drill: Acquiring secondary acreage becomes more competitive

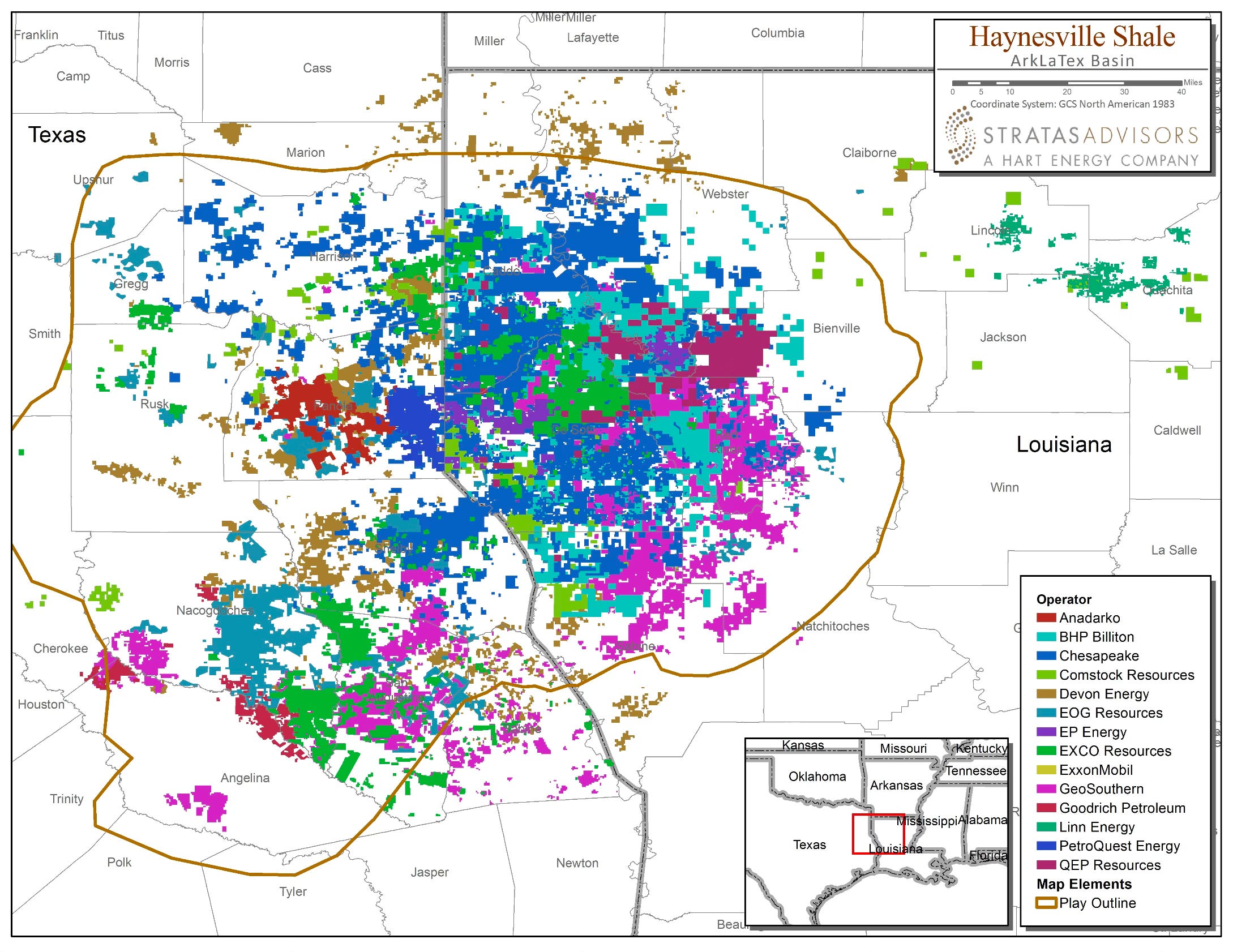

Haynesville acquisitions turn “cut throat” amid land scarcity

Competition for Haynesville Shale mineral rights has intensified dramatically as the basin's core acreage is increasingly locked up by major players, Hart Energy reports. Executives describe the current environment as a "knife fight for on the ground deals," with Live Oak Resource Partners' CEO Andrew Keene noting that "there's a finite pool of willing sellers in the Haynesville, and it's being continuously depleted."

Abu Dhabi's Adnoc Said to Weigh Bid for $9B Aethon Assets. (Rigzone)

The scarcity has pushed acquisition prices higher and forced buyers into a "cost of capital game" for competitively tensioned assets, particularly those with permits or DUCs (drilled but uncompleted wells). In response to the land squeeze, producers are pursuing creative strategies, including moving into the basin's exterior flanks and geologically complex areas such as the Natchitoches fault zone.

This pivot comes as falling drilling and completion costs—down to $1,300-$1,400 per lateral foot from $1,700-$1,800 previously—make previously marginal areas more economical. Meanwhile, rapid consolidation means that the top five operators control over 70% of the market share, making Haynesville the second-most consolidated shale play, as producers position themselves to capitalize on rising natural gas prices and growing Gulf Coast LNG demand.

Minerals dealmaking surge expected to define 2025 M&A amid “white space”

Minerals and royalties transactions are projected to surpass $11 billion in 2025, with nearly $6 billion already completed this year, according to Moelis. The market is dominated by Permian deals—headlined by Diamondback Energy's $4.45 billion dropdown to Viper Energy—but also shows growing interest in natural gas assets across the Haynesville, Appalachia, and D-J Basin amid LNG export demand.

The secondary deal frenzy comes as competition for undeveloped "white space" has intensified dramatically, with PE firms aggressively buying unpermitted, undeveloped mineral rights ahead of future drilling.

This once-risky strategy has become mainstream as buyers push into frontier areas like the Dean sandstone in Dawson County years before operators arrive, often paying near-permitted prices for unpermitted acreage. Industry experts note that the arbitrage opportunity has largely disappeared as the entire minerals market matures, with Viper’s Austen Gilfillian observing that "mineral guys are willing to push the boundaries a little bit more before the operators are," particularly in emerging play areas where first-movers can secure significant returns.

The contradiction of AI investment and data degradation

Majors AI partner investments quietly go operational

While certainly a buzzword, AI in O&G is quietly going from theoretical investments to field-proven results. This week, Nabors Drilling and Corva AI launched RigCLOUD, an “integrated AI drilling intelligence solution”. The platform is just the latest in a series of O&G consultants, OFS, independent, and major projects to reach production.

Yet the buzzy sounding system has already powered the industry's first fully automated drilling operations in Oman and Iraq through Nabors' partnership with Halliburton.

Collide Energy raises $5 million having signed 6,000 users in public, private, and PE-backed producers. (Hart Energy)

Even the government is joining in: Trump orders agencies to speed up NEPA reviews with technology. (E&E News)

The deployment reflects a broader industry focused on AI, with GlobalData's survey showing 80% of oil and gas companies now prioritize AI investments over competing technologies like robotics and Big Data. Declining interest in the latter presents a painful irony though, as very few E&Ps have the data infrastructure needed to properly train and realize field value from AI applications.

Layoffs at EIA raise risks of ‘data darkness’

As oil majors pour resources into AI and data analytics, foundational government data infrastructure faces risks to continuity and quality due to ~40% of the U.S. Energy Information Administration's 350-person workforce accepting recent buyouts under the Trump administration.

Sources indicate the agency is now assessing which of its influential publications—including weekly oil inventory reports that routinely move global markets—it can maintain with dramatically reduced personnel. Several research programs have already been paused and on regular reports are facing modification or curtailment.

Market analysts are concerned about the potential loss of these independent data sources which are relied on by energy traders and producers for over two decades. Critical government data is increasingly being dropped, declining in quality, or manipulated across key markets across the world, reducing confidence and clarity at a time when both are in short order for decision makers.

In Other News:

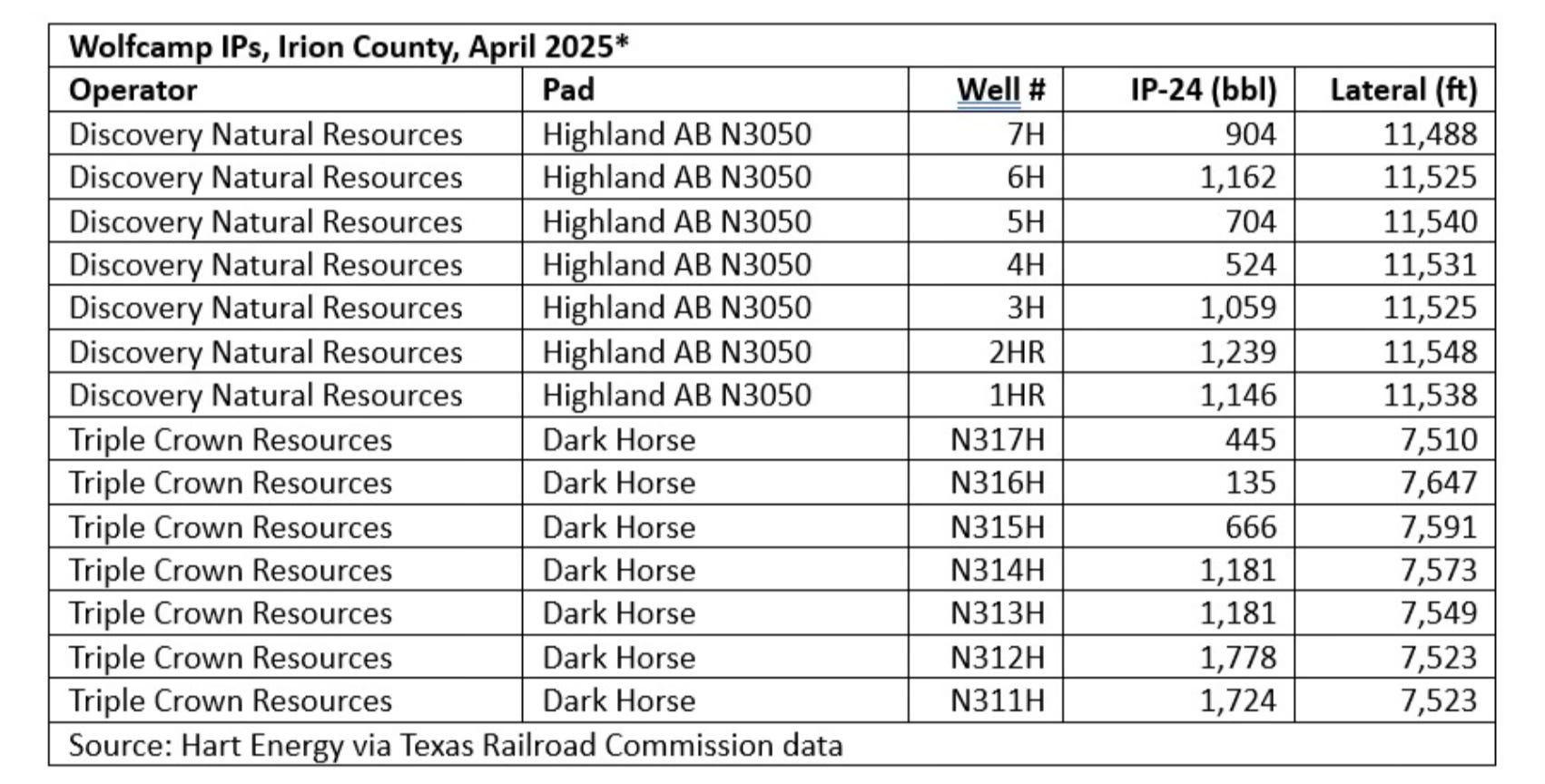

Marginal Midland counties see boost in drilling performance

Once overlooked Permian plays are seeing strong production gains as scarcity-led development yields results. Irion County in the southeastern Midland has already matched its entire 2024 well count in just the first quarter of 2025, with average IPs well over 1,000 boe/d per well.

The Dean formation across Martin and Howard counties is emerging as a critical new zone, with Diamondback, Oxy, and SM delivering productivity ranging from 1,162-1,805 bbl/d. This is a timely development as 32% of Dean acreage remains economic even at $50/bbl while traditional Wolfcamp inventory is "increasingly played out."

Industry begins to bristle amid the size and speed of policy changes

U.S. oil executives are openly challenging the Trump administration's recent economic policy shifts as crude prices have plummeted to $61/bbl, their lowest level since early 2021. Incoming Diamondback CEO Kaes Van't Hof leveled criticism of "self-inflicted" market turmoil and even publicly challenged Energy Secretary Chris Wright on social media.

USEDC buys 20,000 net Permian acres permian with another $600mn in the tank for ‘25 acquisitions

U.S. Energy Development Corporation has executed the largest acquisition in its 45-year history, purchasing approximately 20,000 net acres in Texas' Reeves and Ward Counties for $390 million. The purchase includes substantial proved producing assets and multi-year drilling inventory, and will see USEDC operate a dedicated drilling rig on the newly acquired acreage as part of its ambitious $1 billion investment plan for 2025.

Stat of the Week: Thousand Club

46%

Year-over-year rise in the share of 1,000 boe/d wells drilled. A majority of wells could hit the “thousand club” threshold in 2025 according to Bernstein data.

What We’re Reading:

Expand Energy Joins EQT in Triple-Investment-Grade Credit-Rating Club. (Hart Energy)

Eagle Ford natural gas production increases as crude oil production holds steady. (EIA)

DC Circ. Nixes Environmental Challenge To $44B Alaska LNG Project. (Law360)

Weather, not Trump, spurred Quebec’s power shutoff to New England in March. (Politico)

DOGE Comes for Clean Energy, Putting Exxon and Occidental Projects at Risk. (Wall Street Journal)

US fosters deeper energy cooperation and explores new partnership opportunities in DOE visit to Abu Dahbi. (EnergyConnects)

Upstate New Yorkers Have Given Up $11,000 Per Capita in GDP Thanks to A Fracking Ban. (Thoughts about Energy and Economics)