Upstream Intel 4/28/25

Land shortage > price collapse for slowing M&A | Capex cuts | Battered Bakken | Interior Department eases drilling on the margin

Welcome back to Upstream Intel, Lease Analytics’ weekly roundup of our analysis and insights. As always, we would love to hear from you with news ideas, feedback and anything else you find interesting.

Sent this by a friend? Sign up here to receive UIW in your inbox.

Data Drill: Separating Negative Sentiment from Downturn Defensiveness

Shale responds to falling prices

Shale producers have rapidly cut activity as oil prices hover around $62 per barrel. Smaller independents and majors alike are pushing some package of reducing capex, slower drilling, and corporate restructuring.

The industry's response reflects concern about volatility more than absolute price levels, with uncertainty around tariffs and trade policy creating potential for swift price movements in either direction.

While fear is in the air, this is the discipline which has turned shale producers from spendthrifts into reliable value creators over the past ten years. As one upstream executive noted, producers today are "better prepared to weather an industry downturn than they were in the past."

Identify the right cause of decelerating M&A

This week, Amplify’s 287k acre D-J basin acquisition became the first deal canceled on the back of market uncertainty. Enverus added to the chorus of concerning news with a proclamation that Q1’s 17bn in M&A would be the high water mark as activity is expected to fall for the rest of the year.

However, M&A activity is not $60 oil’s first victim (capex cuts are discussed below). Instead, the decelerating activity is driven from structural asset shortages. Smaller than expected divestiture activity and record land prices in core and secondary basins are to blame.

The energy land shortage had already crimped dealmaking and sent capital into the mineral and royalties market before the price drop. This odd combo of structural shortages and a bearish price cycle creates a "standoff between sellers reluctant to unload their assets at a discount and buyers already stretched by M&A valuations."

“It’s a good time to be moving ahead, buying acreage and getting ready for the next cycle.”

— Michael Oestmann, CEO of Midland-based Permian producer, Tall City IV Exploration, which is planning to drill in late 2025 and early next year

Yet a growing minority of operators already see the volatility the cuts as an opportunity to position for the inevitable rebound, demonstrating how the industry's hard-won financial discipline has created companies strong enough to capitalize on downturns rather than merely survive them.

PE firms are still raising new funds to go after upstream assets, and gas players are still more limited by the number of attractive opportunities in a market with a smaller pool of scalable, high-quality private assets compared to what was in the Permian a few years ago.

Getting restructuring right

“Jekyll and Hyde” restructuring: spending cuts while integrating

E&Ps are aggressively cutting costs as oil prices hover near $60 in a market where, as one executive noted, "$70/bbl is the new $50/bbl" for profitability. Matador is dropping rigs and Ring Energy has slashed quarterly spending by 50%. Beyond reduced spending plans, producers are restructuring with Conoco announcing layoffs and Devon unveiling a well-received plan to generate $1 billion in annual cash flow improvements by 2026.

The hedge fund Elliott is turning up the heat on BP with a demand for deep spending cuts. (FT Energy Source)

These cuts come as companies are still integrating major acquisitions made during better price environments. Devon's new CEO has pivoted from M&A to optimizing existing assets, while ConocoPhillips is centralizing operations after absorbing several companies including Marathon, Shell's Permian assets, and Concho Resources.

The danger lies in distinguishing between trimming excess and cutting essential operational capacity. Wall Street is watching closely to ensure promised acquisition synergies materialize. Producers must carefully balance immediate financial relief against long-term value creation that justified these acquisitions. Excessive cuts risk undermining integration benefits already priced into valuations, potentially transforming these Jekyll-and-Hyde restructurings from short-term solutions into long-term value destruction.

Efficiency and innovation persuade banks to stick with E&Ps

Energy lenders remain eager to deploy capital despite oil price volatility, with substantial capacity available following the recent consolidation wave, according to four oil bankers who spoke to Hart Energy. Banks now view themselves as longer-term partners through market cycles, impressed by producers' capital discipline and efficiency gains that were absent during previous downturns—making them more willing to fund the industry even during downturns.

Unlike 2014 when many banks retreated from the sector, today's lenders express confidence in energy companies' fundamentals. Over a decade of capital discipline has also bought the second good will with bankers:

"We're hungry. We're ready to do business," states Comerica's Jeff Treadway, reflecting a banking sector that views the current slowdown as temporary rather than structural. First Horizon's Moni Collins appreciated how producers can now "maintain or grow production with less investment than say 10 years ago."

In Other News:

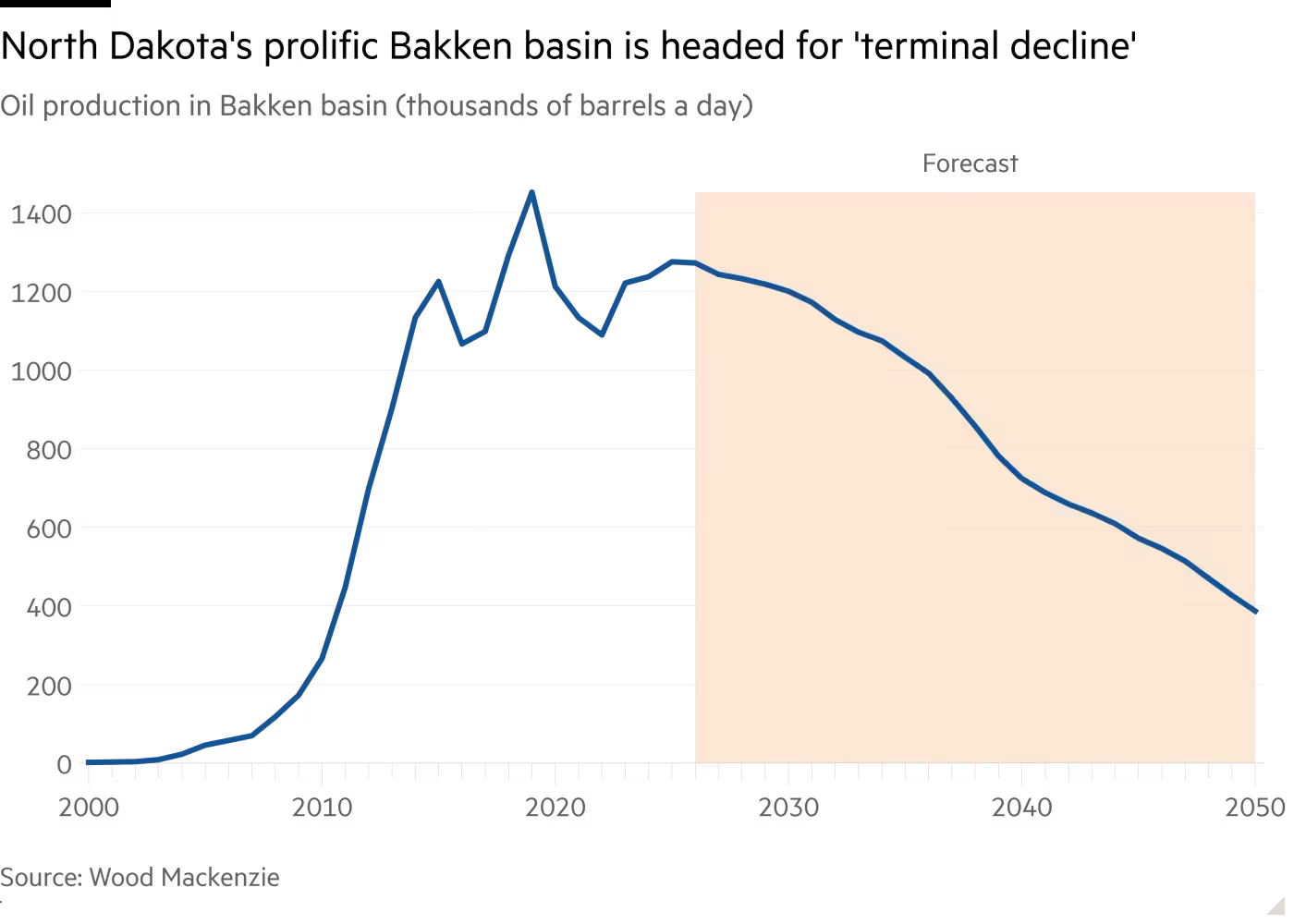

Market volatility and a structural slowdown hit North Dakota shale

North Dakota's oil industry faces mounting pressure from price volatility, the third-largest oil-producing state has significantly higher breakeven prices ($50-60 per barrel) than the Permian ($38-42). State officials warn of "terminal decline" without technological breakthroughs like carbon dioxide enhanced oil recovery, while local officials in Trump-supporting counties express concern about potential job losses and cuts to infrastructure projects heavily dependent on oil tax revenues.

Majors cut costs by outsourcing engineering

Major oil companies are increasingly shifting specialized white-collar positions to India amid industry-wide cost-cutting, the Wall Street Journal reports. Chevron added 600 positions in India as part of a new $1 billion engineering hub — while cutting 8,000 jobs — with similar moves by Exxon, Shell, BP, and TotalEnergies. These companies are hiring engineers, geologists and scientists in India at roughly one-third the cost of their U.S. counterparts, while U.S. oil and gas employment has declined nearly 15% since mid-2019.

Interior Department makes promised deregulatory moves

DoI is implementing emergency permitting procedures that will slash approval times for energy and mining projects to a maximum of 28 days. The department has simultaneously moved to reduce the size of national parks to open more lands to development while allowing offshore producers to drill from multiple reservoirs at higher pressure differentials. Officials see the colocation rules increasing Gulf of Mexico production by as much as 10% or 100,000 bpd by 2035.

With tariffs triggering $60 oil, it’s hard to see who will seriously benefit from the deregulation though. Legal experts also caution that such dramatic reduction of environmental reviews will lead to extensive court challenges.

Quote of the Week: ‘Delay, baby, delay.’

The oil industry has ingrained institutional knowledge from the price crashes in 2015 and 2020 and is ready to act swiftly in a downturn. While the US administration targets both lower prices and ‘Drill, baby, drill’, we’re more likely to see ‘Delay, baby, delay.’

— Fraser McKay, head of upstream analysis at Wood Mackenzie

What We’re Reading:

Crescent Energy completes sale of $83MM in non-operated Permian basin assets. (World Oil)

Oxy’s Hollub: EOR Essential to Energy Security as Oil Supply Peaks. (Hart Energy)

TETRA Technologies announces expansion of smackover formation evergreen unit and update on additional test well results. (Oil and Gas 360)

APA Reveals 2,700 bbl/d Test Results from Sockeye-2 in Alaska. (Hart Energy)

The Oil Patch’s ‘Manhattan Project’: How to Fix Its Gargantuan Water Problem. (Wall Street Journal)

Texas Upstream Employment Slips in March, TIPRO Says. (Hart Energy)

Shakedown federalism and energy policy nationalization. (Brookings Institution)