Upstream Intel 5/12/25

Peak production? | A&D heat up offers a win-win | Independents position defensively | Breaking down breakeven prices | BP explores sale

Welcome back to Upstream Intel, Lease Analytics’ weekly roundup of our analysis and insights. As always, we would love to hear from you with news ideas, feedback and anything else you find interesting.

Sent this by a friend? Sign up here to receive UIW in your inbox.

Data Drill: Structural warnings, cyclical positioning

Smart energy observers predict peak oil…again

Diamondback Energy CEO Travis Stice joined the long line of peak oil declarations, warning that U.S. production has peaked as crude prices plunged 20% in April. The top 10 E&P responded by slashing $400 million from its budget and dropping three rigs.

Diamondback is a smart shop, but smart money has bet against U.S. oil before and lost. The Midland Petroleum Museum’s display of premature "peak shale" headlines, shown above, reflects the trap of betting against shale.

More A&D is a win-win, if E&Ps have their assets ready to swing

Far from preparing for a collapse in U.S. production, E&Ps were busy this week as asset deals surged, with nearly a dozen transactions by UIW’s count. In a down cycle, A&D is becoming a win-win: over-leveraged E&Ps get to shed assets and de-risk balance sheets, while well-capitalized independents and private equity players selectively reload with premium inventory.

APA, still digesting its $4.5 billion Callon Petroleum acquisition, shed $608 million in non-core New Mexico assets — less than 5% of its Permian oil production. That’s strategic trimming: debt reduction for the seller, and capital-efficient opportunity for buyers like Permian Resources, which picked up inventory with $30 WTI breakevens that can compete for capital today.

PE–backed Crescent is playing both sides, reportedly marketing over $1 billion in non-core assets across multiple basins to concentrate firepower on lower breakeven positions in Eagle Ford and Uinta. On the other end of the spectrum, EOG used the downturn to fill in strategic “holes” in its acreage, enabling longer laterals and better capital efficiency.

This is what being a swing producer demands: clean, contiguous assets you control outright. The ability to “hit the gas” when prices rise only works if your portfolio is already aligned. Fragmented or legacy-heavy positions can’t move fast enough.

As Permian Resources’ Will Hickey put it, the downturn could actually “pick up” A&D as more sellers get motivated. That opens the door for disciplined independents to “thread the needle” by maintaining output with less capital today while setting up for aggressive growth when prices rebound.

Independents position more defensively

Independent producers cut capex, wells, and target new cost savings

As Texas drilling permit applications fell 28% month-over-month to their lowest level since February 2021, operators are focusing on high-grading inventories and accelerating efficiency programs rather than sacrificing valuable production volumes.

Independents are intensifying cost-cutting measures beyond their initial Q1 reductions, with Diamondback slashing an additional $400 million (10%) from its budget, EOG trimming $200 million, Devon cutting $100 million, and Civitas reducing spending by 8%—all while maintaining 2025 production guidance.

The sector has established clear price thresholds for further activity reductions, with Coterra identifying $50 oil as its "tipping point" for deeper cuts, while Devon would take "more aggressive actions" if prices remain in the "low $50s."

EOG reflects a microcosm of independent E&Ps’ Q2

EOG’s moves this week illustrate the balance between defensiveness and strategic positioning that defines today’s independents. The producer is cutting $200 million from its capital budget and reducing drilling by 25 wells across mature basins—yet simultaneously deploying $275 million to acquire 30,000 strategic Eagle Ford acres described as "the unicorn left in the play."

CEO Ezra Yacob articulated the company's philosophy amid falling prices: "We're more focused on generating returns and free cash flow than on delivering volume growth in what looks like a potentially oversupplied market."

Unlike previous downturns when producers slashed activity indiscriminately, today’s disciplined independents are high-grading their portfolios—cutting wells in mature areas while EOG increases activity by 20% in emerging plays like Uinta and Dorado.

This selective approach to capital allocation, combined with opportunistic M&A during price weakness, enables the company to maintain its counter-cyclical readiness, supported by what management describes as "excess cash on the balance sheet" for potential acquisitions.

In Other News:

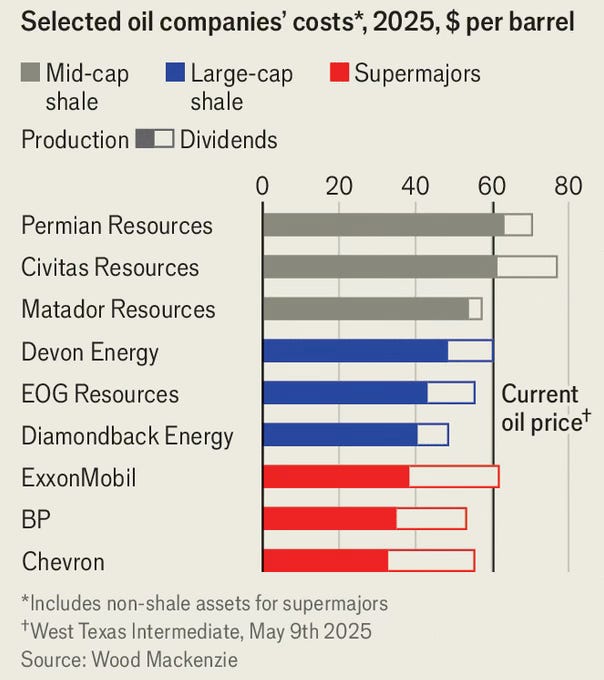

The break even price fallacy

As "break-even" prices get thrown around, the average metrics cited from Fed aggregations are being misunderstood. OPEC+ nations require $50–$125 per barrel to fund government budgets, while U.S. independents operate with operational break-evens in the $26–$45 per barrel range.

Without government spending to account for, E&Ps’ break-even prices reflect strategic corporate choices rather than simple production economics. U.S. break-evens levels vary widely—from $26 per barrel for existing Eagle Ford wells to $85 per barrel for aggressive growth drilling.

Rather than a unified global oil market, OPEC+ fiscal requirements, Wall Street financial objectives, and basin-specific cost structures have created multiple overlapping markets—each responding to different price signals. This fragmentation allows many producers to generate substantial free cash flow even at prices that supposedly fall below "break-even" thresholds.

Shell explores purchasing struggling BP

Shell is evaluating a potential acquisition of BP with advisers, reportedly waiting for further declines in BP’s stock before moving forward. A deal would create an energy titan producing 5 million barrels per day and controlling a quarter of the global LNG market.

Despite BP’s assets being valued at nearly twice its current £57 billion market capitalization—following a 30% share price drop—Shell CEO Wael Sawan has publicly signaled a preference for share buybacks over acquisitions. Still, ExxonMobil, Chevron, TotalEnergies, and Abu Dhabi’s Adnoc are also reportedly examining potential bids for the 116-year-old British major.

House energy lawmakers push to supercharge federal leasing

The House Natural Resources Committee is advancing sweeping oil and gas legislation that would mandate 30 Gulf of Mexico lease sales over 15 years, six offshore Alaska sales, and four auctions in the Arctic National Wildlife Refuge. The measure is being pushed through as part of a budget reconciliation bill expected to bypass Democratic opposition in the Republican-controlled Senate.

Industry groups, including the Independent Petroleum Association of America, have praised the initiative as a “welcome and long-overdue step.”

Quote of the Week: Playing Politics

“Some analysts suspect Riyadh’s real aim is to hand Trump a welcome gift in the form of cheap oil, in the hope of building stronger security ties with Washington.

— Bloomberg Energy on suspicions that Riyadh's shift is less about OPEC overproduction - which is only about half a million bpd - and more about politics

What We’re Reading:

Oil Wells Per Location in Lower 48 US States More Than Double in Past Decade, EIA Says. (Reuters)

What’s Next for the US as an Apex Hydrocarbon Producer? (Hart Energy)

Oil Gains From Four-Year Low on Signs US Output Is Set to Fall. (Bloomberg)

WoodMac: US tight oil faces tariff cost pressures, but increases will be offset elsewhere. (Oil and Gas Journal)

Occidental Petroleum’s shares have slumped 22% this year as U.S. oil prices come under pressure. (Wall Street Journal)

Silicon Valley’s ‘Move Fast and Break Things’ is Making an Administrative Mess in Washington. (Hart Energy)

Senate panel considers Trump’s EIA pick; EIA braces for staff cuts that could hinder data. (Oil and Gas Journal)

Puerto Rico drops $1B climate lawsuit after Trump DOJ sues states over legal challenges to oil and gas industry. (Politico)