Upstream Intel 6/23/25

Haynesville vs Australia | Banks raise O&G lending | "Pent-up" portfolio rationalization | XTO lease lawsuit | Horseshoe wells boost economics in tight leaseholds

Welcome back to Upstream Intel, Lease Analytics’ weekly roundup of our analysis and insights. As always, we would love to hear from you with news ideas, feedback, and anything else you find interesting.

Sent this by a friend? Sign up here to receive UIW in your inbox.

🕒 Read time: 4 minutes

Data Drill: International Investment Intrigue

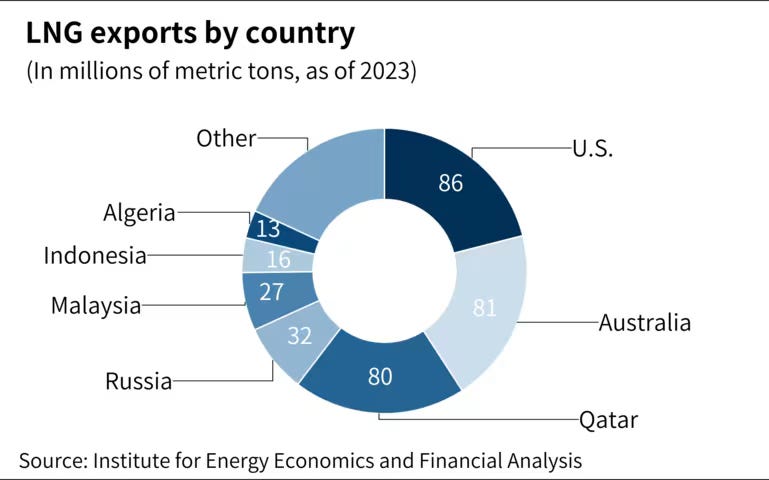

Why Mitsubishi looks at Haynesville while ANDOC chose Australia

Mitsubishi’s pursuit of Aethon’s Haynesville gas assets for roughly $8 billion and ADNOC’s separate $19 billion play for Australia’s Santos capture a deeper strategic pivot: Asian and Middle Eastern energy giants are moving from passive stakes to full control of upstream gas supply. For buyers whose economies depend on stable LNG imports, the lesson of recent price spikes and AI-driven power demand is clear — own the wells, not just the offtake.

The two deals show a sharp divergence in strategy. Mitsubishi favors Aethon because Haynesville gas sits right next to the Gulf Coast’s expanding LNG corridor, offering immediate volume, mature decline profiles, and scale that slots into Japan’s tight long-term supply plans. ADNOC, after weighing Aethon, preferred Santos: more undeveloped reserves, clearer political support for Pacific LNG growth, and a foothold in Asian supply chains where Abu Dhabi’s longer-term ambitions for gas dominance fit better.

Both moves point to a larger wave ahead. Asian buyers, flush with cheap capital and underwriting these assets over 20-year flow horizons, routinely value mature production higher than most U.S. strategics do. They are willing to “overpay” for stable cash flow over speculative drilling upside. That math means more deep-pocketed bids for private shale and LNG feedstock are likely, as they hedge supply security while Western peers remain more cautious.

But American players aren’t locked out. Domestic E&Ps and their private equity backers still excel at turning underdeveloped acreage and complex gathering systems into margin machines, a skill foreign buyers rarely match. As global buyers raise the floor for acreage prices, U.S. drillers with rock knowledge and midstream leverage can still outbid rivals where there’s hidden upside to unlock.

Turning back on the financial taps

Banks increase upstream spending for first time since 2021

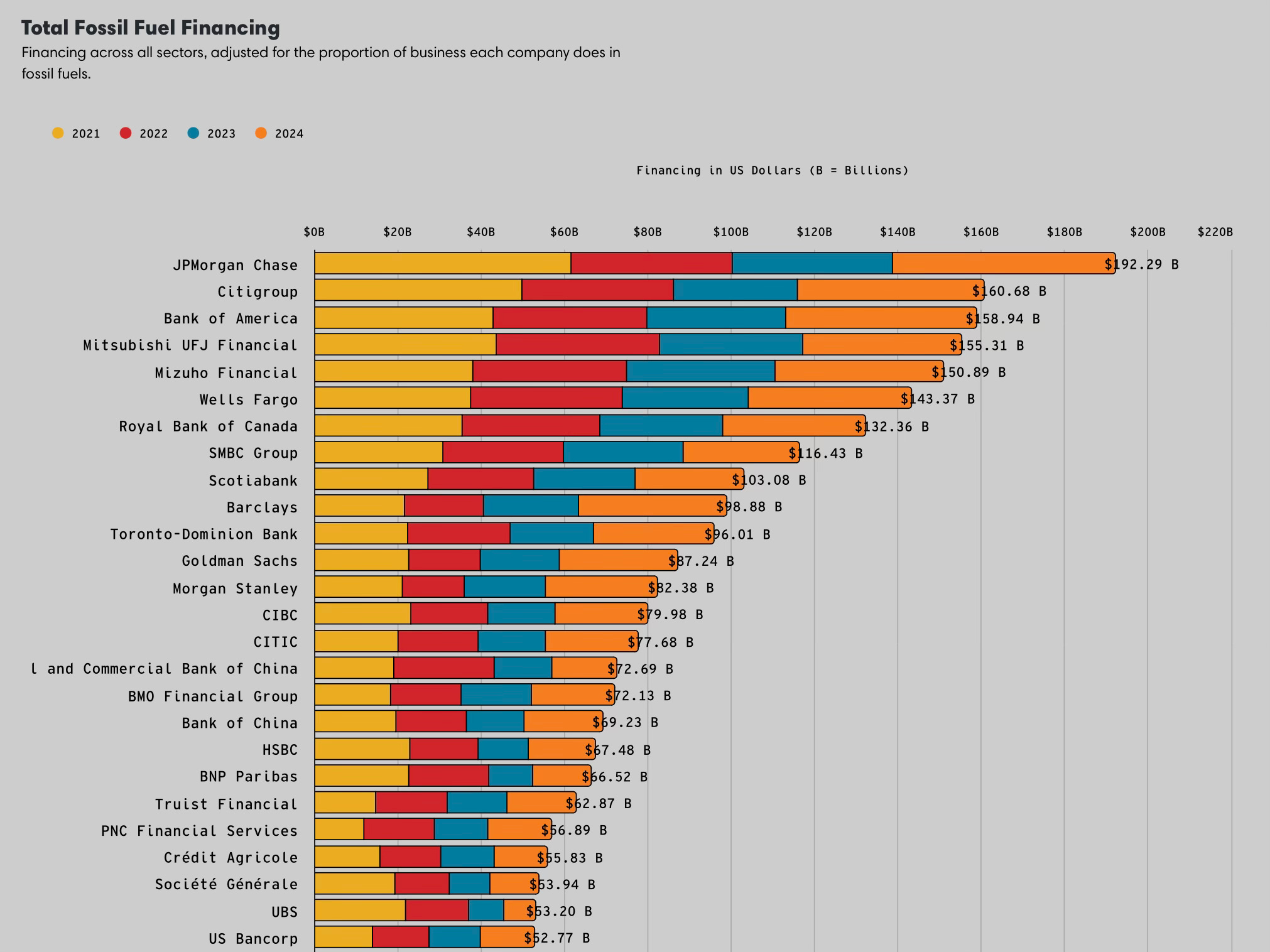

You wouldn’t know it by reading headlines, but financiers are increasingly confident in oil and gas. Big banks boosted upstream and broader fossil fuel spending for the first time since 2021, with total financing up more than 20% last year to $869 billion. Loans, bonds, and acquisition funding all rose sharply as U.S. lenders in particular pulled back from net-zero pledges and faced political pushback for curbing fossil lending.

American banks led the charge: JP Morgan, Citigroup, Bank of America, and Barclays posted the biggest absolute jumps, with U.S. firms alone supplying a third of all fossil capital. After years of shareholder and regulatory pressure to limit fossil exposure, banks are now leaning back in, a sign that political and energy security shifts are once again driving upstream credit flows.

Upstream M&A expected to recovery in H2 25 on pent-up inventory

Upstream M&A is widely expected to rebound in the second half of 2025 as companies finally move to offload the piles of non-core assets they’ve been sitting on since the last wave of megadeals.

April’s tariff shock and shaky oil prices didn’t kill deal appetite, they forced sellers to delay processes and buyers to push back on aggressive pricing. The result was a lull, with billions in dry powder and undeployed equity stuck waiting for clearer signals.

That clarity is coming and the logic for portfolio clean-up is stronger than ever: capital must be focused on optimizing core holding, not scattered fringe positions.

Private equity funds, reloaded with record war chests from Pearl, EnCap, Quantum and others, are lining up to buy precisely these carve-outs. Stronger gas fundamentals — from AI data center demand to restored LNG export momentum — mean valuations are holding up for the right assets. In short, the backlog can’t last much longer: upstream A&D is gearing up for a busy finish to 2025.

In Other News:

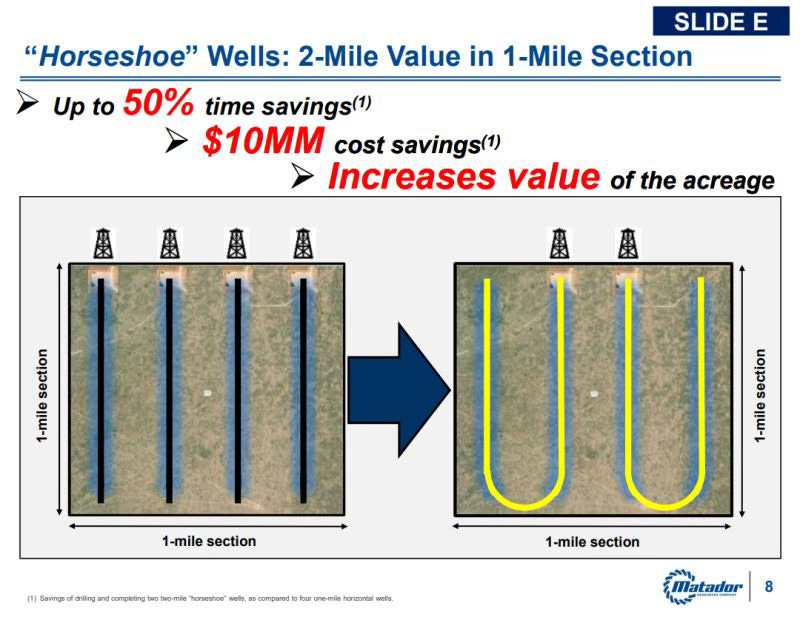

Horseshoe Wells boost economics in tight leaseholds

Horseshoe, or “U-lateral,” wells are giving operators a cost-effective way to tap tight or irregular leaseholds that once limited longer laterals, boosting returns on what was once low-priority acreage. By looping wells back on themselves, producers like Matador, Vital Energy, and Comstock are cutting drilling costs by millions and squeezing more production from squeezed footprints, turning stranded tracts into profitable assets and reshaping how Tier 2 and Tier 3 lands are valued.

Chevron buys lithium leaseholds

Chevron has entered the U.S. lithium sector with its first leasehold acquisitions in northeast Texas and southwest Arkansas, picking up 125,000 net acres in the Smackover Formation from TerraVolta Resources and East Texas Natural Resources.

Following Exxon’s lead, the oil major plans to tap its subsurface and brine expertise to develop a domestic, commercial-scale lithium business using direct lithium extraction (a faster, lower-footprint alternative to hard-rock mining) to secure critical minerals for the energy transition and future-proof its portfolio if oil demand wanes.

XTO lease holders pursue class action exposure for overarching

XTO Energy is trying to block hundreds of Appalachian royalty owners lawsuit against purported padding gathering and processing fees, and underpaying gas royalties. XTO’s economists argue the leases differ too much in royalty math and post-production terms to meet Rule 23, and that the challenged fees were in fact the lowest on offer in the basin.

A ruling on certification [Kriley et al. v. XTO Energy Inc. (W.D. Pa. 2:20-cv-00416] will decide whether XTO faces a sprawling statewide fight or a scatter of individual suits—worth tracking for anyone negotiating deductions into new leases.

Quote of the Week:

“The world is rushing into the age of AI with a 20th century grid, 19th century permitting systems and 18th century policies”

Sultan Al Jaber, head of the Abu Dhabi National Oil Company on the energy infrastructure and regulatory challenges facing AI investments.

What We’re Reading:

Oil Price Surge Sparks Burst of Hedging Among Shale Drillers. (Bloomberg)

Southwest Gas completes sale of Centuri Holdings shares. (Offshore Technology)

Wyoming Governor: Bet on Powder River Oil to Beat Market Challenges. (Hart Energy)

World Oil Demand to Keep Growing this Decade Despite 2027 China Peak, IEA Says. (Reuters)

USGS: Huge Oil Reserves Under Federal Land in Alaska, New Mexico. (Hart Energy)

Goldman estimates geopolitical risk premium of around $10 per barrel for Brent after prices rise. (BOE Report)

US Senate proposes $1bn tax break for oil and gas developers. (Offshore Technology)

US DoI proposes expansion of oil and gas development in Alaska. (Offshore Technology)

Changing the salinity of frac fluid in a reservoir may boost EOR efforts, according to a research paper presented at URTeC. (Hart Energy)