Upstream Intel 6/9/25

Uinta and Utica attract investment | Oil industry reaches a new equilibrium | Interior pushes for more Arctic leasing | E&Ps consider geothermal

Welcome back to Upstream Intel, Lease Analytics’ weekly roundup of our analysis and insights. As always, we would love to hear from you with news ideas, feedback, and anything else you find interesting.

Sent this by a friend? Sign up here to receive UIW in your inbox.

🕒 Read time: 6 minutes

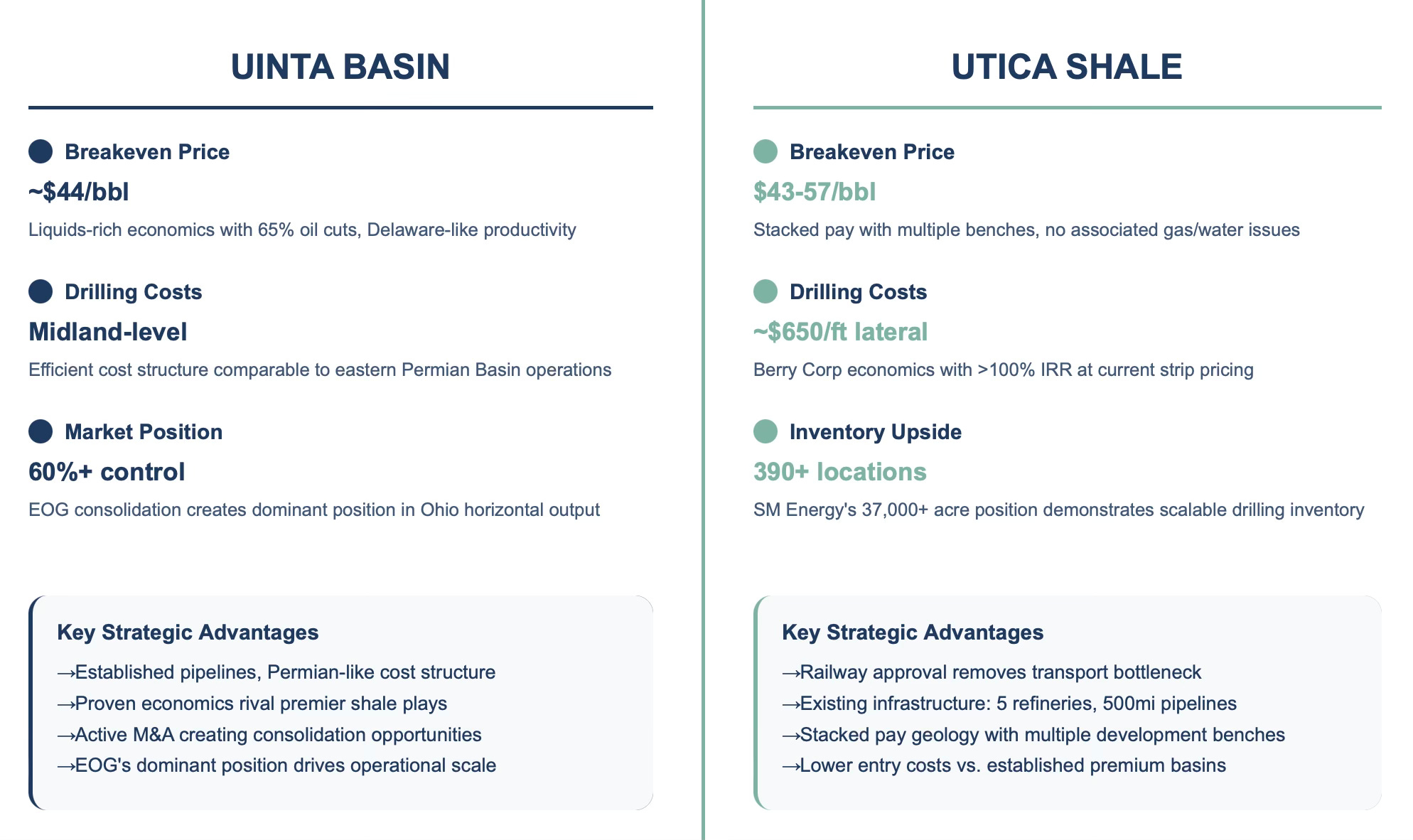

Data Drill: U-shaped opportunity

As prime acreage prices show no sign of easing — in any macro environment — E&Ps are executing a pivot first flagged in this newsletter as early as March 2024: targeting more accessible “secondary” plays. Non-core rock offers solid economics and consolidation upside without the sticker shock of the Permian or other premium basins.

This pivot is creating a “U-shaped” trend, reflecting both the shape of the horseshoe laterals that boost well productivity and the renewed focus on the Utica Shale in Ohio, and the Uinta Basin in Utah.

Advances in drilling technology, improved infrastructure, and more competitive breakeven costs are driving these plays to the forefront, especially as the Haynesville joins the Permian as mostly “bought-up” basins. With Tier 1 inventory becoming scarce, these emerging basins offer a critical path to growth for operators eager to secure scale and production at lower entry costs.

Utica: From Emerging to Essential

EOG Resources’ $5.6 billion acquisition of Encino Acquisition Partners made headlines, but the real story is how the deal signals a broader consolidation wave reshaping Ohio’s Utica.

EOG now controls 61% of the state’s horizontal oil output, and the remaining 43,382 barrels per day are drawing interest from operators seeking scale, including Ascent Resources (considering an IPO), Infinity Natural Resources (fresh off a $265 million offering), and Gulfport Energy, whose CEO has openly flagged Ohio M&A plans.

The play’s appeal extends beyond consolidation. Analysts have dispelled the bear case that oil cuts “fall off a cliff,” with decline rates comparing favorably to four other major oily shale plays.

KeyBanc’s analysis of 577 wells in the Utica highlights promising results, while the liquids-rich economics and premium gas exposure to Gulf Coast markets, via firm transportation capacity, create multiple value drivers for operators willing to build positions.

Uinta: Infrastructure Breakthrough Unlocks Growth

A few states over, the Supreme Court’s green light for the 88-mile Uinta Basin Railway has reignited interest in a region long constrained by high transport costs. New rail capacity and expanded local refineries are spurring operators like Berry Corp and SM Energy to ramp up drilling programs, with costs around $650 per lateral foot proving competitive.

Berry’s shift from declining California to rising Utah is already paying off, with returns exceeding 100% at current strip pricing. As regulatory hurdles fade and infrastructure strengthens, the Uinta is stepping into the spotlight as a cost-effective growth play for operators looking to diversify beyond the Permian and secure oil-rich acreage in a region with significant upside.

A New Upstream Equilibrium

Acclimating to noise: Financiers show comfort with long-term upstream prospects

Even amid trade policy uncertainty, banks and energy financiers are showing steady confidence in the long-term fundamentals of upstream markets. The latest Haynes Boone Energy Bank Price Deck Survey trimmed its 2025 oil price forecast to $58.30/bbl but left its 2035 outlook essentially unchanged—signaling a belief that recent price volatility won’t derail the sector’s structural supply-demand balance.

Natural gas projections echo that sentiment: banks lifted near-term forecasts to $3.50/MMBtu but still expect prices to settle back into the low $3 range beyond 2026 as supply growth matches demand. “It’s a vote of confidence in market fundamentals,” says Haynes Boone’s Kim Mai. This ability to separate short-term noise from long-term opportunity reflects a more mature phase in the sector, where lenders are comfortable funding steadier growth over sharp booms and busts.

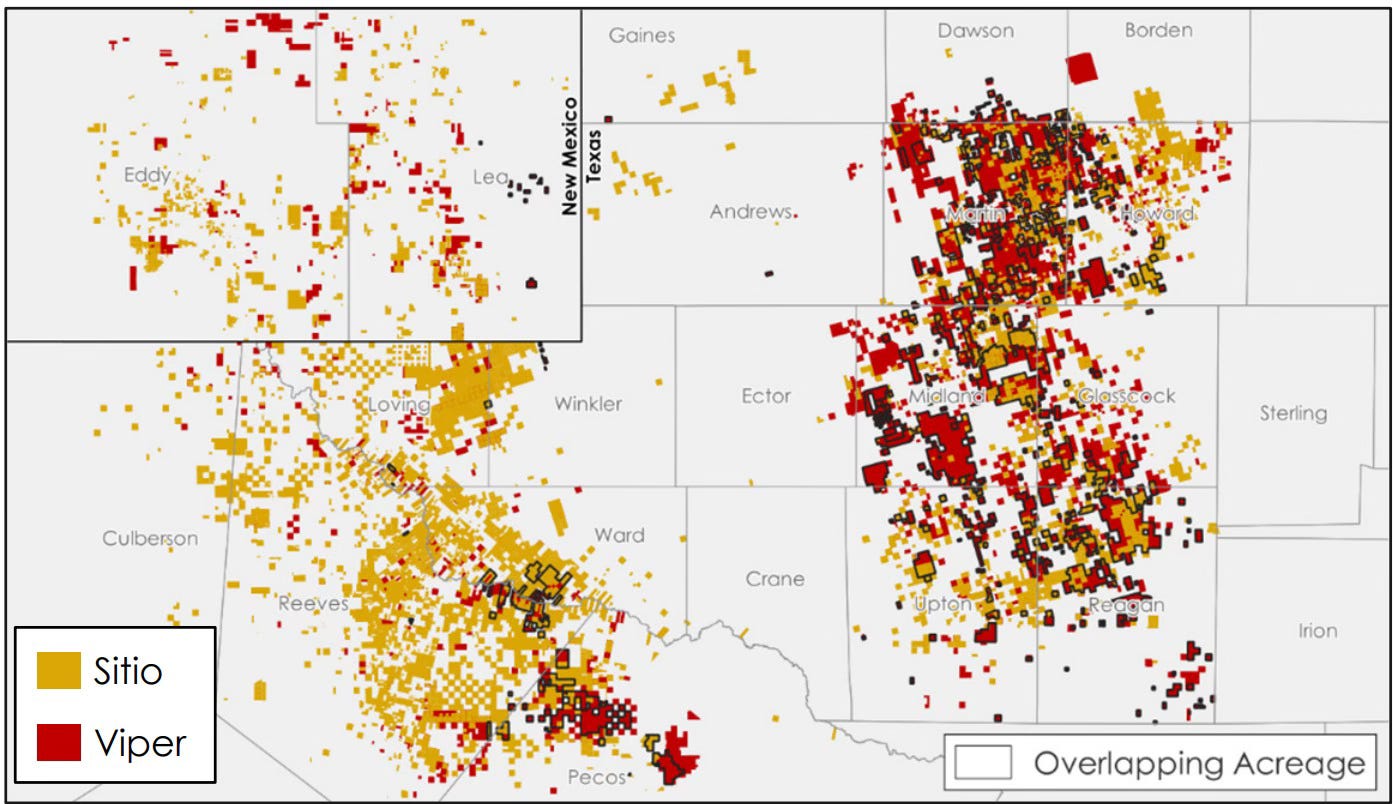

Strategic Expansion: Viper buys Sito Royalties for $4.1bn

Viper Energy’s $4.1 billion acquisition of Sitio Royalties is an example of this more disciplined mindset. The all-stock transaction—Viper’s second major move this year—extends its minerals and royalties footprint across key basins, especially the Permian, where Diamondback continues to drill.

By focusing on overlapping acreage and cost efficiencies rather than opportunistic grabs, Viper is building a platform that balances low breakevens with reliable cash flow. This approach mirrors a broader shift toward more deliberate growth strategies that align with a new equilibrium, one that prizes resilience and strategic fit over expansion at any cost.

Geopolitical Ripples: Canadian firms exit U.S. as Ottawa questions energy integration

Vermilion Energy’s $88 million sale of its Powder River Basin assets marks another sign of the sector’s evolving strategic calculus. By exiting the U.S. market, Vermilion is refocusing on Canadian and European gas-weighted assets, aligning with Ottawa’s push to strengthen domestic energy independence while reducing exposure to U.S. trade volatility.

This decision reflects a growing awareness that geopolitics now shapes upstream strategies as much as geology. As North America’s integrated energy model comes under strain, operators are re-evaluating cross-border ties and prioritizing national alignment.

Vermilion’s move signals that the upstream sector is adjusting to a new equilibrium—one defined by the need to navigate both global markets and domestic policy headwinds with greater caution and resilience.

In Other News:

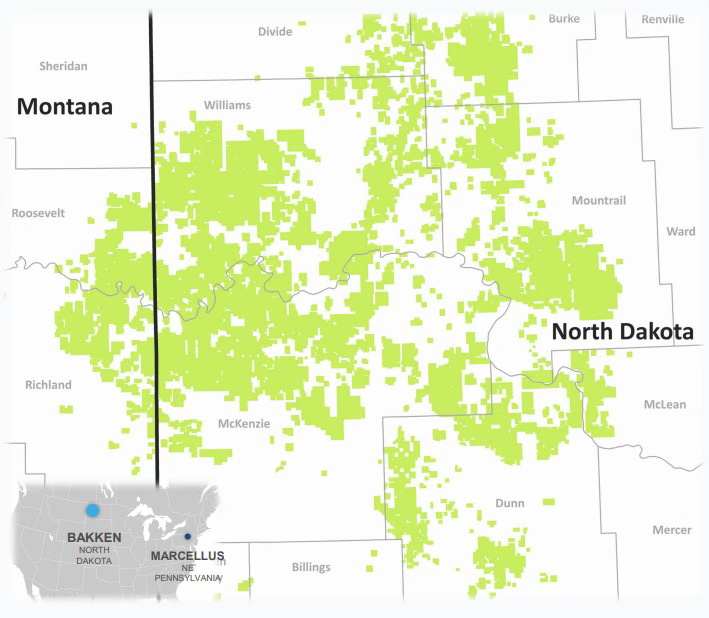

Advanced techniques extend the Bakken’s long plateau

The Bakken continues to sustain its production plateau 25-years after the shale revolution began, as operators leverage 4-mile laterals to reduce breakeven costs by $8–12 per barrel and unlock previously uneconomic acreage on the basin’s fringes, Hart Energy explores.

Operators are prolonging the basin’s productive life through recompletions of legacy leases, advanced permitting strategies, and efficiencies that now enable a single rig to match the productivity of three or four rigs from a decade ago.

Operators explore geothermal business lines

Oil and gas producers in the Gulf Coast, Midcontinent and Rockies are exploring geothermal energy opportunities on existing assets, leveraging their drilling expertise and infrastructure to tap into strong geothermal gradients and diversify revenue streams as traditional inventory declines.

While Devon and Chevron have invested in geothermal startups, analysts note that most oil and gas interest remains exploratory despite the Trump administration’s move to fast-track geothermal projects with emergency permitting procedures.

Trump moves to lift lease limits on Arctic drilling

The Interior Department has moved to roll back Biden-era restrictions that protected nearly half of Alaska's National Petroleum Reserve from oil and gas drilling. The 23-million-acre NPR-A contains an estimated 8.7 billion barrels of recoverable oil and could see production climb to 139,600 barrels per day by 2033.

The rollback is the latest move in the administration’s early efforts to streamline federal land use for resource extraction, reflecting a shift from conservation-focused policies toward maximizing energy development on public lands.

Quote of the Week: Losing exploration for ‘flipping’

“Exploration is not a lost art, but it’s not like it was prior to the Bakken discovery and the manufacturing mode that a lot of people went into. Prior to that, exploration was something that every oil company had, practically.

There were a few people that were flippers and primarily just dealt with M&A. But most companies had a large degree of exploration and a lot of that has been lost.”

— Harold Hamm, Founder and Chairman of Continental Resources

What We’re Reading:

ONEOK’s $940MM Deal Takes Full Control of Delaware G&P JV. (Hart Energy)

Jadestone appoints Little as CEO: Little holds over 30 years of experience in the upstream oil and gas industry, the majority of which was with Marathon Oil Co. (Oil and Gas Journal)

Terra Team Launches New E&P with $300MM in Kayne Anderson Backing. (Hart Energy)

The OPEC+ Production Boost May Have a Bigger Bark Than Bite. (Bloomberg)

Tight oil production in Permian drives growth in onshore U.S. Lower 48 states production. (EIA)

BP appoints former U.S. shale boss to board as part of strategy shift. (Bloomberg)

Cactus to Acquire 65% of Baker Hughes’ Surface Pressure Control Business. (Hart Energy)